You know you need landlord insurance. The only issue? Landlord insurance is confusing — especially trying to find the right policy. Two common policy options you’ve probably come across are dwelling policy 1 (DP1) and dwelling policy 3 (DP3).

But, what are the differences between those two policies? And how do you know which one is right for you and your property? We’re here to answer your questions. Let's start by taking a look at the differences between DP1 vs DP3.

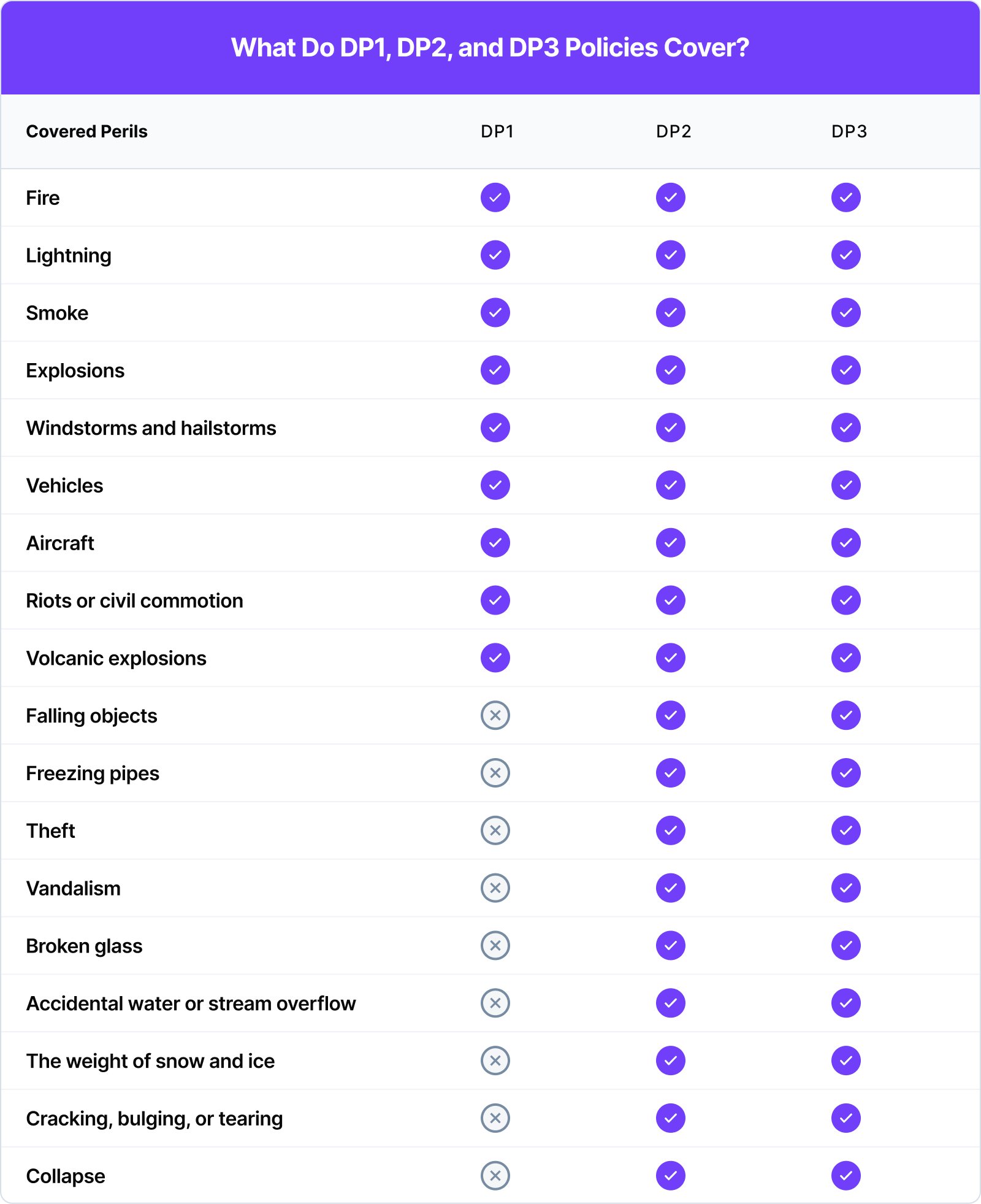

What is DP1 insurance?

DP1 insurance offers the least coverage of the dwelling policies. It is a named peril policy, which means that it only covers the perils explicitly stated in the policy.

These perils typically include damage from:

• Fire and smoke,

• Lightning,

• Explosion,

• Wind and hail,

• Riots, and

• Volcanos.

DP1 insurance typically doesn’t protect against many common damage-causing events including:

• Frozen pipes,

• Roof damage from falling trees,

• Theft, or

• Water damage.

DP1 generally only covers the main structure. However, you can sometimes add surrounding building (also known as other structures on your policy) and personal property coverage to DP1 insurance.

If your property is damaged by a covered peril, DP1 insurance will typically pay actual cash value (ACV) to repair the damage. ACV is the replacement cost minus any depreciation.

So, for example, if your 10-year-old roof is damaged in a covered peril, DP1 insurance will pay you what your 10-year-old roof is worth today — not the cost of a new roof today. This depreciated value is often well below what it costs to fully repair the damage. With DP1 insurance, you may have to pay tens of thousands out-of-pocket to fix any damage.

What is DP3 insurance?

Whereas DP1 insurance offers the least coverage, DP3 insurance offers the most coverage. As such, DP3 insurance is the most popular landlord insurance.

DP3 insurance is an open peril/risk policy. This means it covers all damage-causing events except those explicitly listed in the policy. Some common exclusions you might see are nuclear hazards, war, and mold.

Along with being an open peril policy, DP3 insurance generally includes additional coverage like liability and personal item coverage. With liability coverage, you’re protected if a tenant injury occurs on your property. This coverage means you won’t be on the hook for the tenant’s medical or legal expenses. Many DP3 policies, but not all, will provide some coverage for your personal belongings at the home, such as appliances and lawn equipment.

With DP3 insurance, you can also add loss of rent coverage. A damaging event like a fire or natural disaster could make your property unlivable until it’s repaired. This means you can’t collect rent. If you have DP3 insurance with loss of rental income coverage, your insurance will pay you this lost rent if the damaging event is covered.

For any covered damage, DP3 insurance pays the replacement cost value (RCV) in most cases (an exemption example is in the case of a roof older than 15 years; here, depreciation would be factored in). Instead of paying for the depreciated value, RCV pays the current market rate for materials needed to repair your property. With DP3 insurance, you could receive the full amount needed to make any repairs — potentially saving you tens of thousands in out-of-pocket costs.

Do I need DP1 or DP3 insurance?

Now that you know some of the differences between the policies, you’re probably wondering which one is right for you.

Reasons to choose DP1

If you’re on a very tight budget, DP1 insurance could work for you. Because it offers less coverage, DP1 premiums are generally lower than DP3 premiums. Just remember, cutting corners on cost now may backfire. If your property is damaged, you’ll end up paying more to repair it.

DP1 insurance could also work for you if you have a vacant property or expect to be without tenants for at least a month. Since there’s no one living in the property to cause damage, you likely don’t need as much coverage. This can make DP1 insurance a good fit.

Reasons to choose DP3

However, if you want the most protection for your property, DP3 insurance is the way to go. It provides protection for the most events. And, DP3 insurances provide additional coverage for liability, personal items, or even loss of rent. Overall, DP3 insurance will protect your property better than with DP1 insurance.

You might also choose DP3 insurance if you want to reduce out-of-pocket costs. Your premiums will likely be higher with DP3 insurance, but the amount you have to pay if your property is damaged is often much lower. That’s because DP3 typically pays RCV for any damages. So, DP3 insurance is the right choice if you want to keep unexpected out-of-pocket costs to a minimum.

DP3 coverage costs more than DP1 because it covers far more. Industry estimates commonly put a DP3 premium roughly 30 to 50 percent higher than a comparable DP1 policy, though the gap varies with property value, location, age, and condition. When weighing the two, compare the premium difference against the out-of-pocket risk of ACV payouts under DP1.

Let's review: DP1 vs DP3

When choosing landlord insurance, you might be stumped on which dwelling policy to choose. DP1 insurance provides the least coverage and is cheaper. DP3 insurance provides comprehensive coverage with the option to add additional coverage. However, DP3 premiums tend to be higher.

We can't tell you which to choose, but we hope this article helps break down the differences in DP1 and DP3. Once you’ve figured out which dwelling policy is right for you, it’s time to get a quote. The easiest, fastest, and most transparent way to get your landlord insurance quote is with Obie.