Renovating a Rental Property? Here’s What You Need to Know About Builder’s Risk Insurance

Whether you’re updating a recently purchased rental, completing a major rehab between tenants, or preparing a property for its next lease, renovations are a common part of owning investment real estate.

But while many investors focus on construction costs, timelines, and contractors, insurance is often overlooked until a lender, agent, or contractor asks an important question:

“Do you have Builder’s Risk coverage?”

The answer depends on the type of work you’re doing.

Some renovation projects can remain covered under a standard landlord insurance policy, while larger projects may require Builder’s Risk coverage to help protect the property during construction.

In this guide, we’ll explain:

- What Builder’s Risk insurance is

- When it may be needed

- How it differs from landlord insurance

- Which renovation projects typically require it

- How Obie can help protect eligible renovation projects

What Is Builder’s Risk Insurance?

Builder’s Risk insurance is temporary property coverage designed for buildings that are actively being built, renovated, or undergoing significant improvements.

Unlike a traditional landlord insurance policy, which is designed to protect an occupied or rent-ready investment property, Builder’s Risk coverage helps protect properties while construction is in progress.

Depending on the policy, Builder’s Risk may help protect against covered losses such as fire, wind, hail, vandalism, theft of certain building materials, and other covered causes of loss during construction. Coverage details vary by insurer and policy. (Avoid overpromising because your coverage specifics differ.)

Builder’s Risk vs. Landlord Insurance

One of the biggest misconceptions among investors is that Builder’s Risk replaces landlord insurance.

It doesn’t.

Think of them as serving two different purposes.

At Obie, eligible renovation projects are supported through Builder’s Risk coverage as part of our landlord insurance offering, allowing investors to maintain appropriate protection while completing significant improvements.

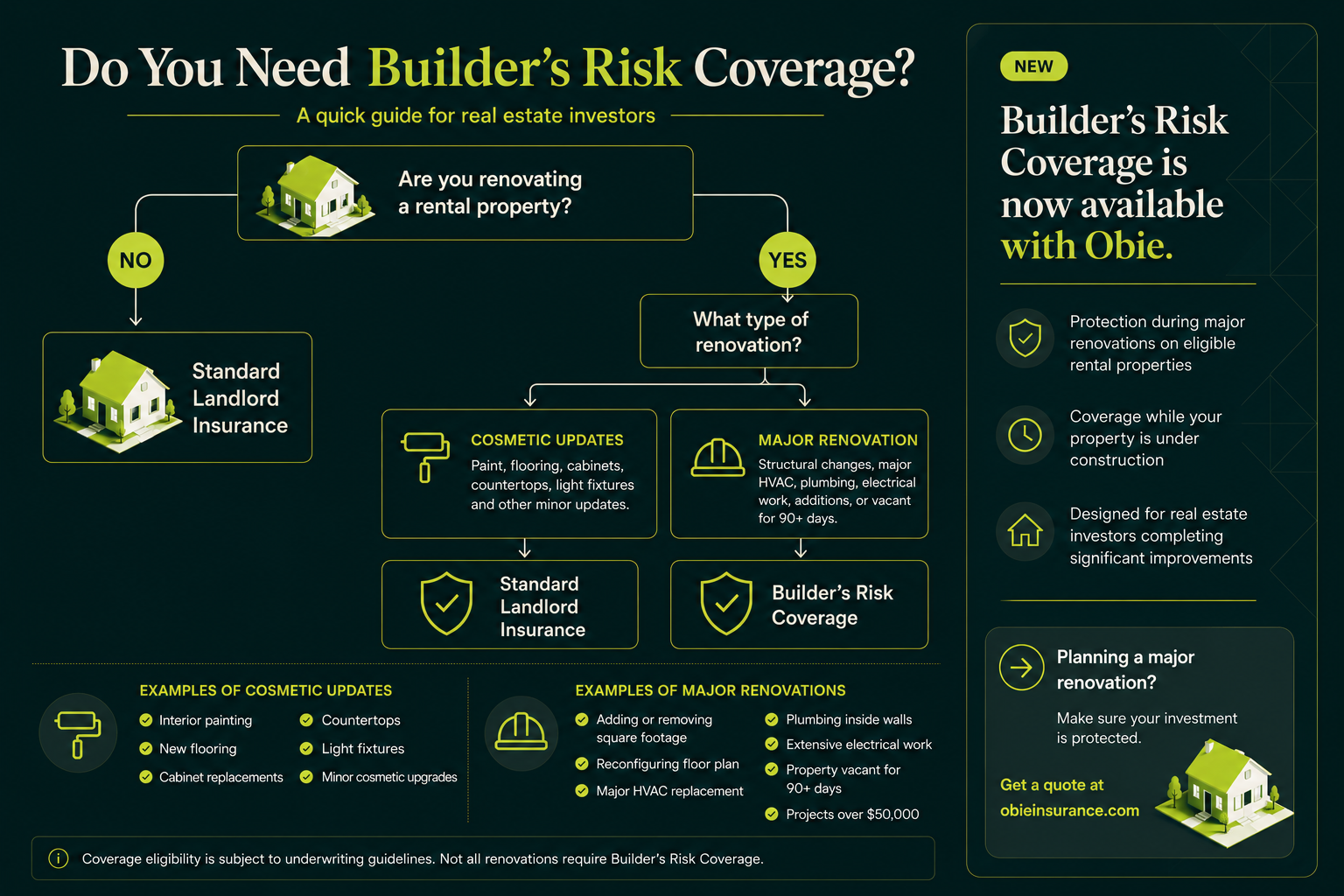

When Do You Need Builder’s Risk Insurance?

The answer comes down to the scope of the renovation.

Cosmetic renovations typically don’t require Builder’s Risk

Examples include:

- Interior painting

- New flooring

- Replacing countertops

- Installing cabinets

- Replacing light fixtures

- Minor cosmetic upgrades

These projects generally don’t significantly alter the structure or major building systems.

Major renovations may require Builder’s Risk

Builder’s Risk is generally appropriate when renovations become more substantial.

Examples include:

- Adding or removing square footage

- Reconfiguring the floor plan

- Major HVAC replacement

- Significant plumbing work inside walls

- Extensive electrical work

- Projects expected to leave the property unoccupied for more than 90 days

- Renovation projects exceeding $50,000 in scope

Why Insurance Changes During Major Renovations

Major renovations introduce risks that typically aren’t present in a stabilized rental property.

During construction, a property may be:

- Vacant for an extended period

- Missing portions of its roof

- Open to weather exposure

- Undergoing plumbing or electrical work

- Receiving deliveries of expensive building materials

- Frequently accessed by contractors and subcontractors

Because of these changing risk conditions, insurance requirements often change as well.

What Types of Investors Benefit Most?

Builder’s Risk coverage can be especially valuable for investors pursuing strategies such as:

- BRRRR (Buy, Rehab, Rent, Refinance, Repeat)

- Value-add renovations

- Major property rehabs

- Fix-and-rent projects

- Significant turnover renovations between tenants

If your investment strategy involves improving properties before generating rental income, it’s worth discussing whether Builder’s Risk is appropriate for your project.

Things to Consider Before Starting Your Renovation

Every insurer has different underwriting requirements, but investors should generally think about:

- The scope of work

- Expected renovation timeline

- Whether the property will be occupied

- Contractor licensing and insurance

- The overall project budget

For Obie, Builder’s Risk eligibility is subject to underwriting guidelines and specific project requirements. For example, qualifying projects generally involve major renovations, must meet minimum project thresholds, and the coverage must be added when the policy is first bound rather than later in the policy term.

Builder’s Risk Coverage Is Now Available Through Obie

We’re excited to expand our landlord insurance offering with Builder’s Risk coverage for eligible renovation projects.

This enhancement allows Obie to support a broader range of investment strategies, helping investors protect qualifying properties during major renovations while continuing to benefit from the speed and simplicity of our technology-driven insurance platform.

Frequently Asked Questions

Does every renovation require Builder’s Risk?

No. Many cosmetic renovations can continue under a standard landlord policy. Larger structural projects may require Builder’s Risk depending on the scope of work.

Can I add Builder’s Risk after my renovation has already started?

Eligibility depends on your insurer’s requirements. With Obie’s current offering, Builder’s Risk coverage must be added when the policy is initially bound and cannot be added later during the policy term.

Is Builder’s Risk only for new construction?

No. It can also apply to eligible existing rental properties undergoing major renovations.

Ready to Protect Your Next Renovation Project?

If you’re planning a major renovation and aren’t sure which type of insurance is right for your investment property, the Obie team can help.

Get a quote today or speak with an Obie insurance specialist to learn whether your project may qualify for Builder’s Risk coverage.