Owning property comes with risk, but the type of insurance you need depends on how you use the home.

If you live in the property, homeowner’s insurance usually offers the proper coverage. But if you rent it out, that same policy may fall short. Landlord insurance is designed specifically for rental situations, offering protections you won’t find in a standard homeowners plan.

While both types cover common issues like fire or weather damage, landlord insurance also helps cover tenant-caused damage, lost rental income, or liability if someone gets injured on-site.

Which one fits your situation? Let’s break down the key differences.

What’s the Difference Between Landlord and Homeowners Insurance?

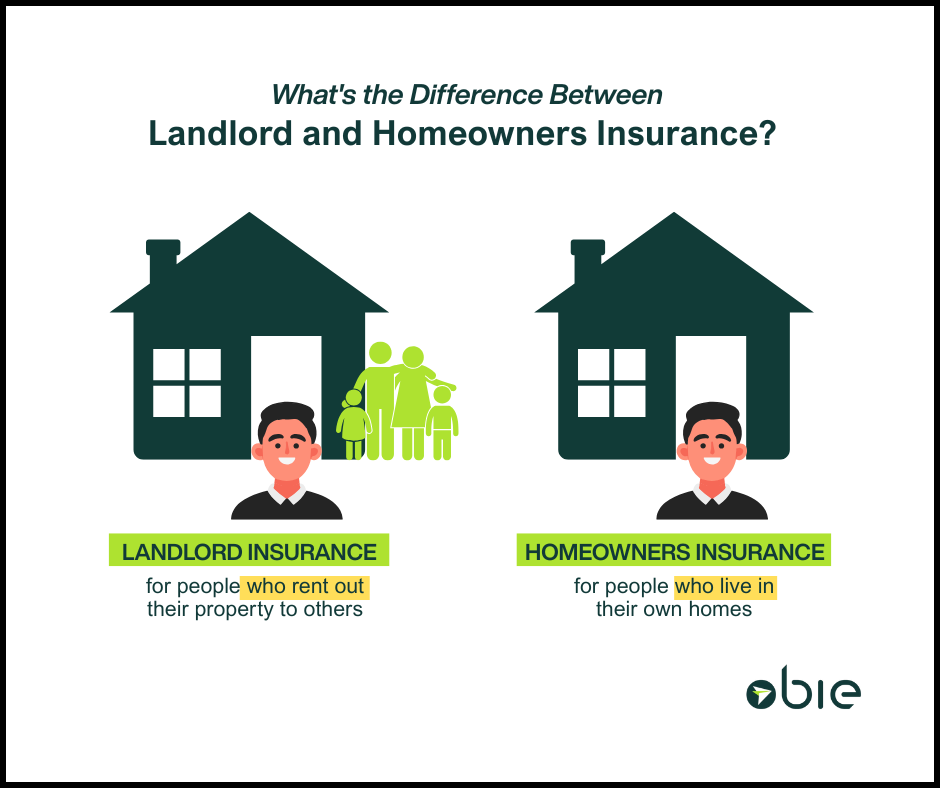

- Homeowners insurance is for people who live in their own homes.

- Landlord insurance is for people who rent out their property to others.

The key difference is who lives in the home. Homeowners insurance protects the owner’s belongings and personal use, while landlord insurance covers rental-related risks like tenant damage and lost rent.

Landlord Insurance vs Homeowners Insurance in Terms of Coverage

Here's the coverage comparison between homeowners insurance and landlord insurance in table form:

Landlord Insurance vs Homeowners Insurance in Terms of Costs

Here’s a clear comparison of landlord insurance vs. homeowners insurance in terms of cost:

Bottom line: Landlord insurance costs more but covers the unique risks of renting out property. It's a wise investment for rental property owners looking for broader protection.

Does a Homeowner Need to Switch to Landlord Insurance When Renting Out Their Property?

Yes. If you move out of your home and start renting it, you must switch from a homeowners policy to a landlord policy. Once your property becomes a rental, most homeowners' policies won’t cover tenant-related claims.

Using the wrong policy can lead to denied claims or even cancellation. Protect yourself by ensuring your coverage matches how you use the property.

Can Homeowners Insurance Be Used for a Rental Property?

No. Homeowner’s insurance is only meant for owner-occupied homes. Once you rent it out, you introduce a new set of risks homeowner’s policies aren’t designed to cover.

Once the home is rented out, the risk profile changes, bringing in tenant-related risks that homeowners policies don’t cover. If your insurer finds out the property is being rented without proper coverage, they can deny claims or drop your policy entirely. To stay protected, you’ll need landlord insurance.

Your Rental Isn't Your Home. Insure It The Right Way.

Renting out your property? Your homeowners insurance likely won’t cover you anymore, and that gap could leave you exposed when it matters most.

Landlord insurance is built to protect your investment, but the traditional process for getting it? Slow, complicated, and often full of guesswork.

Obie changes that.

We make it easy to get the right coverage, with no calls (unless you prefer one) or runarounds, just fast, transparent insurance designed for landlords. You’ll have what you need in minutes to get back to the big picture.

Ready to protect your rental? Get your instant quote from Obie now.

FAQs about Landlord Insurance vs Homeowner Insurance

Can I bundle landlord and homeowners insurance?

Yes. If you own multiple properties, many insurers—Obie included—offer bundling options to help you simplify coverage and potentially reduce your overall cost.

How to cancel homeowners insurance and switch to landlord coverage

Let your insurance provider know you’ve moved out and are renting the property. They’ll cancel your homeowners policy and help you transition to a landlord policy that fits your new needs.

Is landlord insurance more expensive than homeowners insurance?

Generally, yes. Landlord insurance usually costs 15%–25% more because renting out a property brings added risks, like tenant damage and income loss. But that extra cost buys broader protection that homeowners insurance can’t offer.

.png)