Are you faced with the seemingly impossible choice of choosing the best dwelling insurance policy?

You’re not alone. It’s a problem many property owners face, especially those new to property investing. Between understanding all the insurance jargon and analyzing the aspects of every policy, it is not unusual to feel like giving up during the process.

When looking for insurance for your rental property, you will likely come across three different types of policies: DP1, DP2, and DP3. While they all offer some level of protection for your property, they vary in terms of what is covered.

This blog post will break down the key differences between these three types of landlord insurance policies. So, whether you're just starting out as a landlord or are looking to switch policies, read on to learn more!

What is Dwelling Policy Insurance?

Dwelling policy insurance is an umbrella encompassing three different policies. It includes DP1, DP2, and DP3.

Dwelling policies or dwelling fire policies are insurance coverages offered instead of homeowners insurance. Although the name states fire, these policies cover more than just fire peril. They differ in covered perils and exclusions depending on the specific policy.

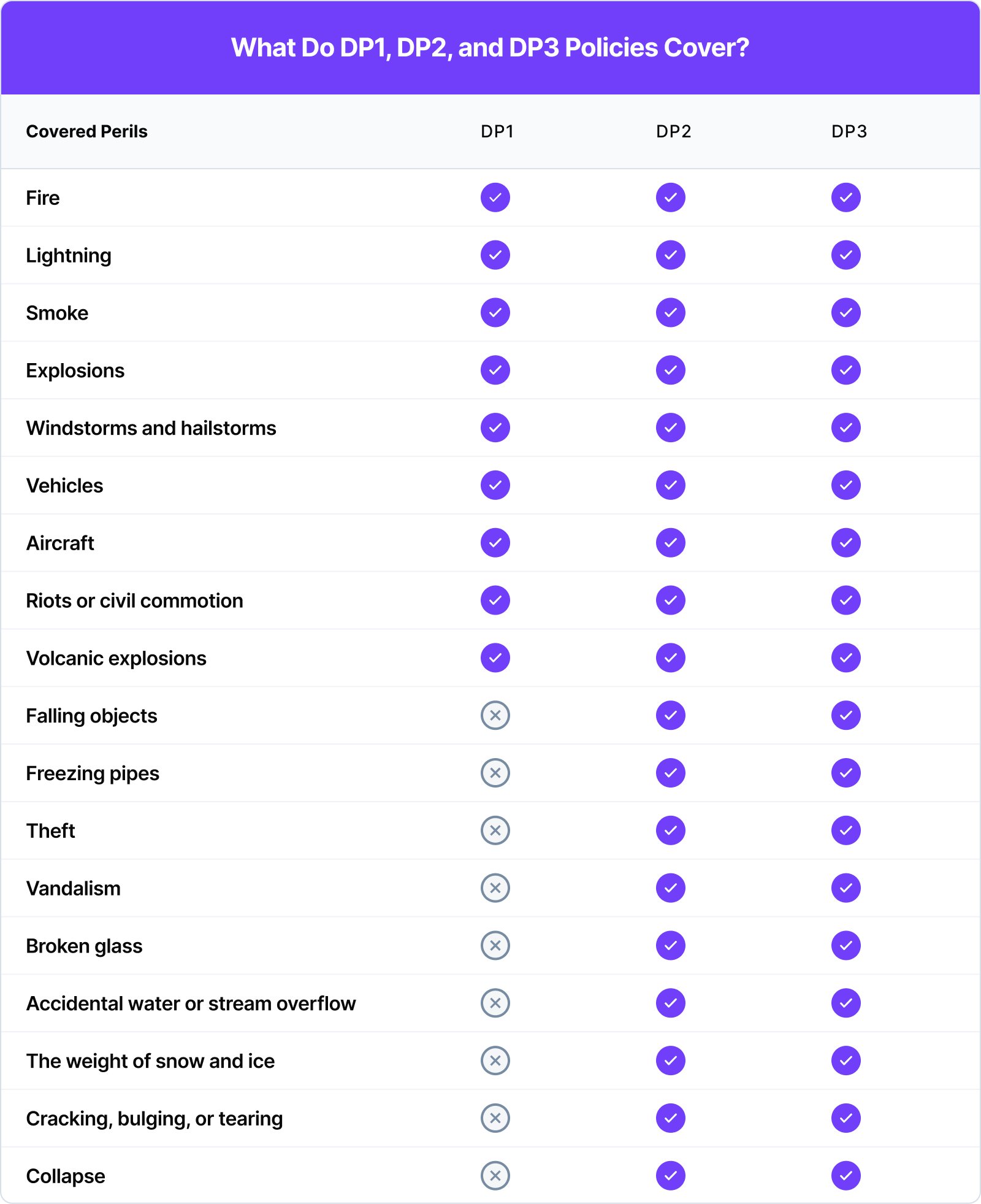

DP1 vs DP2 vs DP3

The main differences between the policies are what is covered and the payout methods.

DP1 and DP2 are both named peril policies, where insurers only cover risks detailed in the policies. The main difference between DP1 and DP2 is that DP2 covers more risks, eighteen in number, while DP1 covers nine. DP 1 is the most basic form of coverage of the three.

For instance, DP2 covers burglary, malicious mischief, freezing pipes, and falling objects, while DP1 does not cover these perils. However, both cover fire, lightning, smoke, riots, and damage from wind or hailstorms (see the below diagram for a comparison of both policies).

On the other hand, the DP3 policy is an open peril policy. It covers all risks except those that the insurer has explicitly excluded. This makes it a more comprehensive policy of the three, providing coverage for more perils.

The DP1 policy is quite different from its counterparts when it comes to payouts. While it uses actual cash value (ACV), DP2 and DP3 payouts are on a replacement cost value basis (RCV). Under the DP1 policy, claim payouts are based on the repair cost minus depreciation. On the other hand, replacement cost value with DP2 and DP3 insurance policies pay the replacement costs for damages using current prices but within the limits of your policy.

For example, if you need to repair damages worth $20,000 on a 10-year-old property, a DP2 or DP3 policy will pay the replacement cost value for these damages. The only cost you will pay is the agreed-upon insurance deductible. But if you had a DP1 policy, you would receive less than $20,000 due to depreciation of the property and have to pay the remaining cost with your own cash.

Another difference between these policies is the cost. DP1 is cheaper as it covers fewer perils, while DP3 is the most expensive. DP2 insurance is in the middle, a more affordable option than DP3 that covers more risks than DP1.

A DP3 policy generally covers everything a DP2 policy does, plus extra coverage. However, there are some perils that a DP3 policy typically does not cover, including:

- Ordinance or Law (aka upgrades to repairs required because building codes and other laws have changed since your property was built)

- Water Backup and Sump Pump Overflow

- Intentional loss

- Mold

- Neglect

- War

- Earthquakes

- Power Failure

- Nuclear Hazard

- Flooding

Basic, Broad, and Special Form Coverage Explained for Rental Homes

A DP1 policy offers basic, named-peril coverage, while a DP2 provides broader named-peril coverage. A DP3 policy gives you the most comprehensive open-peril coverage.

Let's break down the DP1 vs. DP2 vs. DP3 policies to see which one fits your rental home.

DP1: Basic Form Coverage

A DP1 policy is the most basic and cheapest option. It's a "named peril" policy, meaning it only covers losses from a specific list of events, or perils, written in the policy.

- What it covers: Typically includes fire, lightning, and internal explosions. You can often add coverage for windstorms, hail, and vandalism.

- How it pays: It pays out on an Actual Cash Value (ACV) basis. This is the cost to replace the damaged property minus depreciation for age and wear. You get what it was worth, not what it costs to buy new.

- Best for: Vacant properties, landlords on a very tight budget, or older homes where replacement cost coverage isn't practical.

DP2: Broad Form Coverage

A DP2 policy is a step up, offering more protection than a DP1. It is also a "named peril" policy, but the list of covered events is much longer.

- What it covers: Includes everything in a DP1 policy plus other common risks like theft, falling objects, weight of ice and snow, and damage from a sudden burst of your water heater.

- How it pays: It pays out on a Replacement Cost Value (RCV) basis for the dwelling itself. This means it pays the cost to rebuild or repair your rental home with similar materials today, without deducting for depreciation. Your personal property is still usually covered at ACV.

- Best for: Landlords who want more than just basic protection for their rental homes without the higher cost of a DP3 policy.

DP3: Special Form Coverage

A DP3 policy offers the highest level of protection for a rental property. It provides "open peril" coverage for the structure of your home.

- What it covers: "Open peril" (also called all-risk) means the dwelling is covered for everything except for events specifically listed as exclusions in the policy (like war, floods, or earthquakes). Your personal property (like appliances you own) is covered on a named-peril basis, similar to a DP2.

- How it pays: It pays out on a Replacement Cost Value (RCV) basis for the dwelling.

- Best for: The majority of landlords who want peace of mind and the most comprehensive coverage available for their investment property.

Which DP Policy Does a Landlord Need?

The need for any DP policy will depend on your current situation. DP1 is an option if your budget does not allow for a DP2 or DP3 policy. It is also suitable for property owners or homeowners who:

- Have a vacant rental house

- Moved to a different residential home leaving their previous one vacant

- Are waiting for a tenant to move into an empty house

- Have inherited a house but it is vacant as they try to sell it

Unfortunately, DP1 does not provide coverage against vandalism and theft. Vacant homes are more prone to these risks and sometimes squatters. Affordable as it is, it could cost you more in the future if you face any of these risks without insurance.

DP3 policy is best for homeowners renting residential properties only. However, it does not cover residential properties you leave vacant for extended periods, usually 60 to 90 days. These include vacation homes or secondary residences vacant for the better part of the year.

It is also important to keep in mind that most DP2 policies do not provide coverage for properties that remain vacant for extended periods. Why? Because insurance companies term these as higher risk than tenant-occupied residential homes. As such, items needing repair may go unnoticed for an extended time, leading to more significant damages and higher claim amounts.

In addition to covered perils, there is also the aspect of what is covered.

All three policies cover damages to the property’s primary structure and other detached or additional structures, like garages, pool houses, fences, and sheds. DP2 and DP3 will also cover loss of use. This is when you lose rental income when the property is not livable due to any of the covered perils. Finally, DP3 includes personal liability coverage, ensuring you are protected against liability suits if someone gets injured on your property and you are found liable.

.png)

Where to Find a Landlord Insurance DP Policy

There are several alternatives for choosing the best landlord insurance package for your rental property:

Obie: If you’re looking for an easy way to protect yourself and your investment, check out Obie. No paper applications, week-long waits for quotes, or back and forths with brokers.

With Obie, you can get easy, affordable, and transparent coverage for your rental property entirely online through a landlord insurance quote. Furthermore, there are no paper applications to complete and no lengthy waiting periods. On average, landlords save 25% with Obie.

Go here to get an instant quote today.

Brick and mortar insurance agent: You can also search for landlord insurance by checking with your existing insurance provider or broker. This may be the simplest solution because you won't have to conduct much research or compare many quotations from numerous companies.

While providing a simple option, it isn't always the best method to get landlord insurance. Some businesses compete on price by providing limited coverage and terrible customer service when a claim is made.

Other real estate investors: Do you know of a friend or family member who has invested in rental property? Most likely, they already have landlord insurance. They may talk about their experiences with insurers and what they've learned and recommend coverage or a specialist they've worked with.

Networking with fellow landlords: Finding good landlord insurance may be as simple as networking with other real estate professionals on social media or local networking events. In many cases, investor groups may be more than willing to include you as a member.

Final Thoughts

Landlord insurance is a must-have for any property investor. Whether you choose a DP1 policy, DP2 or DP3 will depend on your needs. Each of the available dwelling policies will suit a specific situation.

For example, if you have a vacant property or are on a tight budget, a DP1 policy might be best. This policy is affordable, but it covers limited perils. An alternative to this is the DP2 policy, which covers more risks and is slightly less costly than DP3. Still, it doesn't cover vacant houses and has limited coverage compared to DP3.

DP3 policy is the most comprehensive and usually the most preferred by landlords, despite its higher premium. In addition to the property’s primary and additional structures, DP3 covers loss of income and personal liability.

Before settling on any dwelling policy, it's good to work with a professional insurance broker specializing in landlord insurance. In addition, an online insurance broker like Obie can help ensure you get a policy that meets your specific needs at an affordable price.

FAQs about DP1 vs DP2 vs DP3

Can I switch from DP-2 to DP-3 mid-term without canceling the policy?

Yes, you can usually upgrade your policy mid-term. You don't need to cancel and start over. Contact your insurance agent and ask to "endorse" your policy to a DP-3. Your insurer will calculate the added premium for the rest of your policy term, and your new, broader coverage will begin.

What perils are commonly covered by landlord insurance?

This depends entirely on your policy type:

- DP-1 (Basic): Covers a very short list of named perils, mainly fire and lightning.

- DP-2 (Broad): Covers everything in a DP-1 plus more common risks like theft, falling objects, weight of ice and snow, and certain types of water damage.

- DP-3 (Special): Covers the dwelling for "all risks" or "open perils," meaning everything is covered except what is specifically listed as an exclusion.

Common exclusions on all policies include events like floods, earthquakes, war, and neglect.

How do deductibles work on landlord policies?

A deductible is the amount of money you agree to pay out-of-pocket for a covered claim before your insurance company pays the rest. For example, if you have a $1,000 deductible and a covered kitchen fire causes $8,000 in damage, you would pay the first $1,000, and your insurer would cover the remaining $7,000. Choosing a higher deductible will lower your premium.

Is upgrading from DP-1 to DP-2 worth the extra premium?

For almost every landlord, yes. The upgrade is worth it for two main reasons:

- More Covered Perils: A DP-2 protects you from a much longer list of common problems, like theft or damage from falling trees.

- Better Payout: A DP-2 pays on a Replacement Cost basis for the dwelling, giving you the funds to rebuild at today's prices. A DP-1 only pays Actual Cash Value, which is the replacement cost minus depreciation and may not be enough to cover your repairs.

Can a landlord require tenants to carry renters insurance?

Yes, you absolutely can, and it is a very smart business practice. You can include a clause in your lease agreement requiring the tenant to obtain and maintain a renters insurance policy for the duration of their lease. This protects you because if your tenant's negligence causes damage to your property, their liability coverage can pay for it, which may save you from filing a claim on your own policy.