Slip-and-fall injuries send nearly one million Americans to emergency rooms each year, and the average claim tops $33,000. If that accident happens in your rental, the bill lands on your doorstep—unless your policy is ready. This guide answers the question “does landlord insurance cover tenant injury?” and hands you a step-by-step checklist to seal any coverage gaps before the next rent check arrives.

How is “Tenant Injury” Defined by the Law?

Tenant injury is simply “bodily injury—physical harm, sickness, or disease (including any resulting death)—suffered by a tenant or the tenant’s guest on the insured premises that is alleged to stem from the landlord’s negligence or unsafe property conditions.”

What Counts as a “Tenant Injury”?

As a landlord, you are responsible for providing a safe home, and a tenant injury can happen when something on the property causes physical harm or damages their belongings. Understanding the difference is key to knowing what your insurance may cover.

What’s the Difference Between Landlord Insurance and Renter's Insurance for Injuries?

Landlord insurance pays when a tenant or visitor is hurt and blames the landlord’s unsafe property; renter's insurance pays when the tenant accidentally injures someone else or a guest inside the rental.

Memory aid:

Landlord coverage answers, “Did the property hurt someone?”

Renters coverage answers “Did the tenant hurt someone?”

These two separate safety nets work side-by-side.

Does Renters Insurance Cover Injuries?

Yes, standard policies include landlord insurance liability coverage that pays medical bills, legal defense, and damages when a tenant is hurt by a hazard you should have fixed.

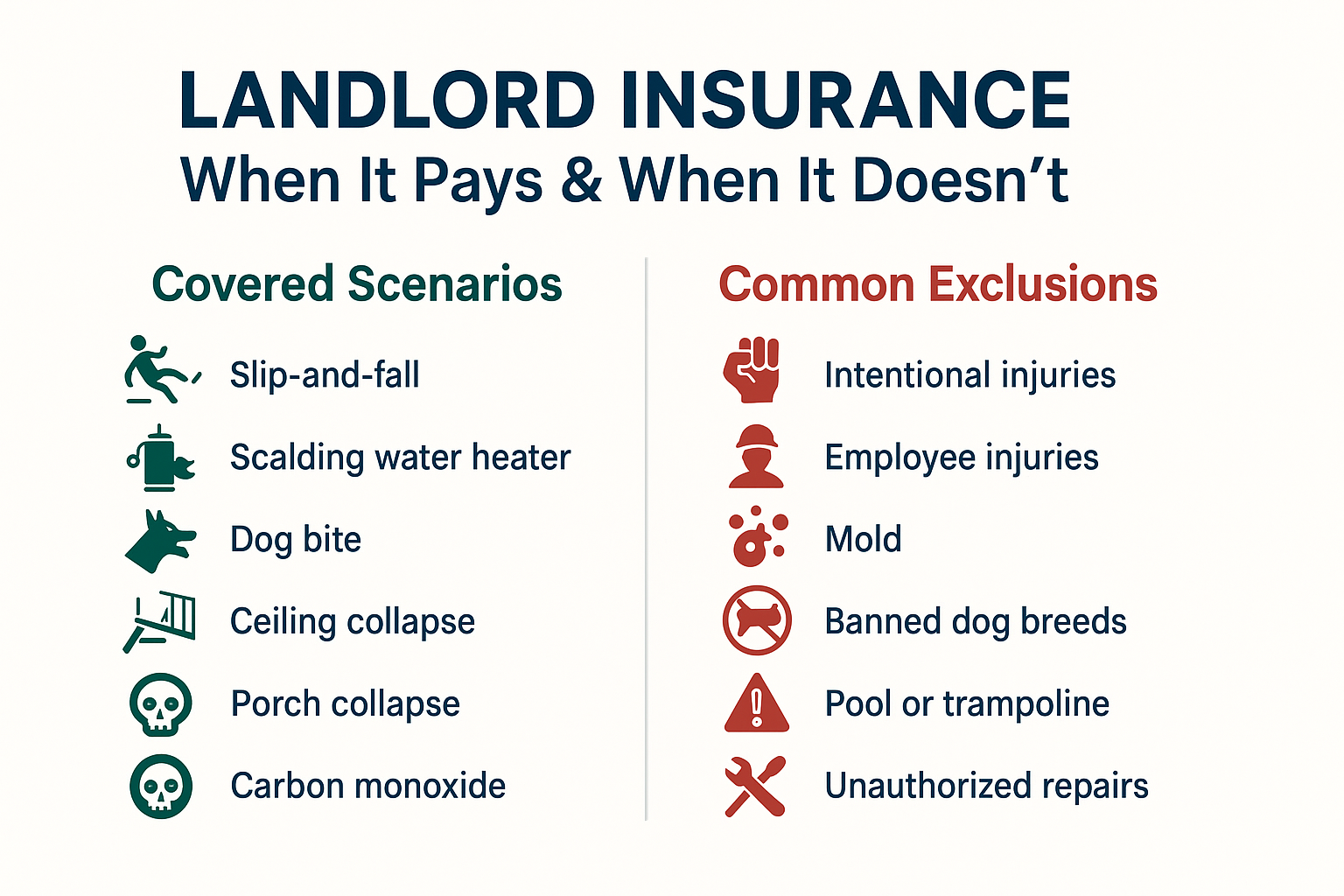

When Does the Landlord Insurance Policy Pay in Tenant Injury Cases, and When Does It Not?

Covered Scenarios

- Slip-and-fall on loose flooring or icy walkways you’re responsible for clearing

- Tenant scalded by a malfunctioning water heater left unrepaired

- Dog bite from a pet you allowed but failed to restrain

- Ceiling plaster that crashes down after an ignored roof leak

- Porch railing collapse from hidden rot you overlooked

- Carbon monoxide poisoning traced to a poorly serviced furnace

Common Exclusions

- Injuries caused intentionally or during an altercation

- Accidents involving employees (handled by workers’ compensation)

- Mold-related illness unless a mold liability rider is in place

- Bites from dog breeds or exotic pets banned in the policy wording

- Pool or trampoline mishaps when required safety fences are missing

- Illness tied to asbestos, lead paint, or radon—environmental hazards require separate cover.

- Injuries after a tenant performs unauthorized repairs or alters the property against lease terms

Who’s Legally Liable with Tenant Injury?

Negligence test (4 quick checks)

- Duty of care: Did you have a legal obligation to keep the area safe?

- Breach: Was that duty ignored or handled carelessly?

- Causation: Did the breach directly lead to the tenant’s injury?

- Damages: Are there medical bills or other losses to pay?

If all four answers land on yes, the liability and the claim fall on your shoulders.

Bottom line: liability follows the party that controlled the hazard and failed to act. Knowing where your duties end and the tenant’s begin helps prevent expensive finger-pointing later.

3 Smart Add-Ons on Your Landlord Insurance Policy

✔ Boost Medical-Payments Limits: Raise the no-fault medical-payments coverage so minor injuries (cuts, sprains) get paid without a lawsuit, keeping goodwill high and legal fees low.

✔ Add an Umbrella Policy: Stack an extra $1–5 million over your base liability to shield personal assets if a severe injury claim blows past standard limits.

✔ Require Renters Insurance: Write a lease clause mandating each tenant carry their policy; it covers their belongings and shares liability, reducing your payout risk and discouraging frivolous claims.

Takeaway Checklist for Landlords

___ Walk the property each quarter and fix hazards right away.

___ Keep written logs and photos of every repair and inspection.

___ Set liability limits at $1 million or higher and add umbrella cover.

___ Insert a renters insurance clause and verify proof at least at signing.

___ Review the policy at renewal to update limits and add needed riders.

Trader Joe’s Car-Crash Lawsuit Shows the Value of Landlord Liability Cover

In Earl M. Hill Family Ltd. Partnership v. Trader Joe’s Co. (Cal. Ct. App., Dec 2024), a car jumped a curb at a Goleta, CA shopping centre, seriously injuring a shopper on the sidewalk. The victim sued both Trader Joe’s (the tenant) and the property’s three landlord entities for US $2.5 million.

- Immediate defence funded: Because the landlords already carried a Commercial General Liability (CGL) policy with Sequoia Insurance, the carrier accepted the tender and appointed counsel, absorbing six-figure legal fees from day one.

- Shared settlement, assets protected: The case settled before trial, with Trader Joe’s and the landlords each contributing US $1.25 million—payments handled through their respective insurance arrangements, not the landlords’ personal pockets.

- Key lesson for owners: Even when a court later finds the landlord partially negligent, robust liability limits and an insurer’s duty to defend can keep a high-stakes injury claim from derailing rental cash flow or forcing asset sales.

Takeaway: Carrying strong landlord liability coverage—and confirming your insurer’s duty to defend—turns a potentially ruinous injury suit into a contained, insurer-managed event.

Need Tailored Protection?

Get landlord insurance built for investors in minutes. Obie’s online platform delivers instant, bindable quotes and tailored coverage so you only pay for what your properties need. Thousands of owners already rely on our service to keep deals moving and claims painless. Ready to shield your rentals? Start your free landlord insurance quote or call +1 (773) 820-7132 to speak with a U.S.-based specialist today.

FAQs about Landlord Insurance and Tenant Injury

Does landlord liability insurance differ from landlord property insurance?

Yes. Liability pays others—medical bills, legal fees, and settlements—when a tenant or visitor blames the landlord’s negligence. Property pays to repair or rebuild the rental structure (and the landlord-owned appliances/furnishings) after a covered peril like fire or storm.

Does landlord insurance cover guest injuries inside a rental unit?

Usually, yes. If a hazard the landlord should have fixed causes the harm, the policy’s liability section can cover medical costs and defence expenses for tenants and their guests.

Is landlord insurance required by law to cover tenant injuries?

No federal or state law mandates it, but most lenders or property managers make coverage a loan or lease condition. Skipping it leaves the owner personally exposed to injury claims.

How do insurers classify “avoidable” vs. “unavoidable” tenant injuries?

It comes down to negligence. Injuries tied to dangers the landlord knew or should have known about are labeled avoidable and trigger liability coverage. “Freak” accidents or harm stemming solely from the tenant’s own actions are deemed unavoidable and typically excluded.