Tenant damage comes with the territory when you own rental property; it’s not a matter of if, but when. In fact, nearly 98% of landlord insurance claims are tied to property damage. That’s why having the right landlord insurance in place is so important. It helps protect your investment from the everyday risks that come with renting, including certain types of tenant-caused damage.

In this guide, we’ll break down what landlord insurance does and doesn’t cover to help you close gaps before your next lease renewal.

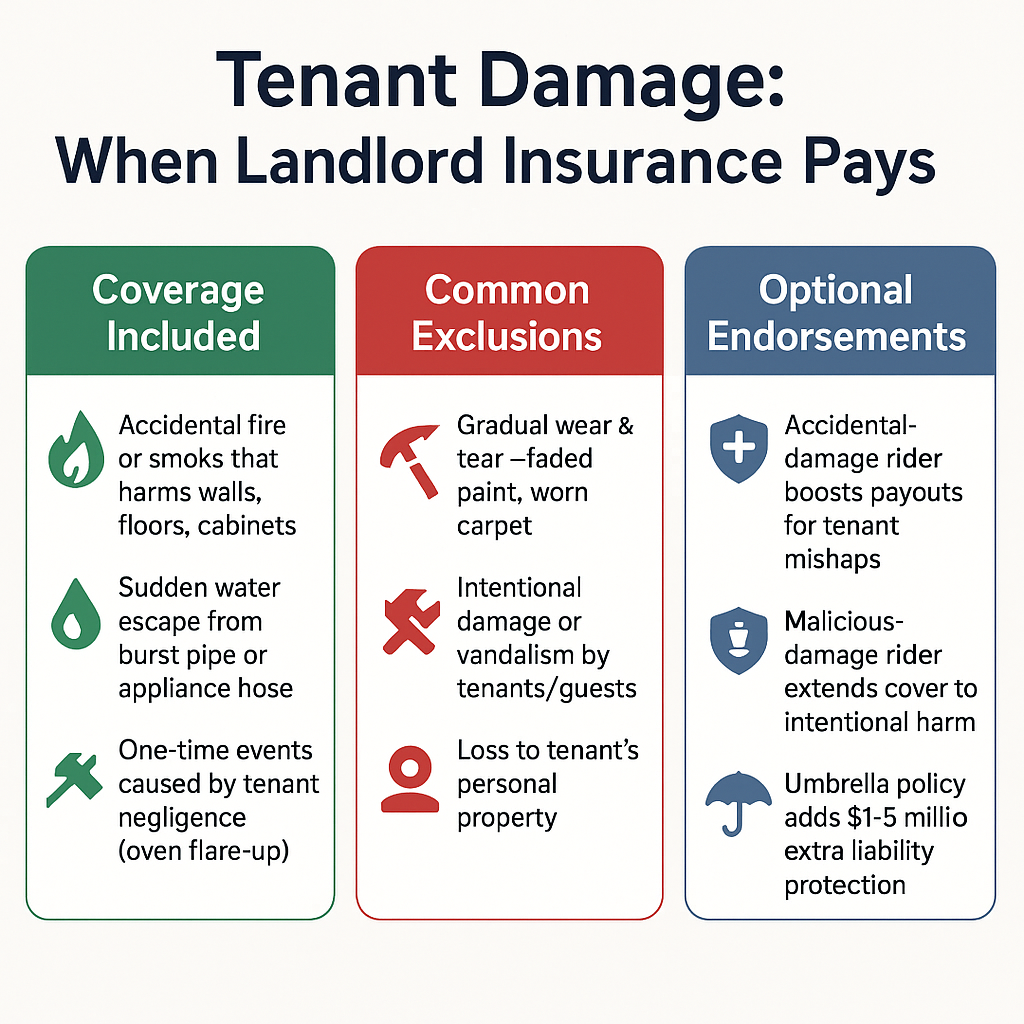

Landlord Damage Coverage at a Glance

What Counts as “Tenant Damage”?

Correctly identifying the difference between tenant damage and "normal wear and tear" is a critical financial and legal distinction for tenant damage.

It is the foundation for making lawful deductions from a security deposit and is key to avoiding costly disputes with former tenants.

Tenant Damage vs. Normal Wear and Tear

- Tenant Damage: This is harm that lowers the value of your property and is caused by a tenant's negligence, carelessness, or intentional abuse. You can typically deduct the cost to repair this from the security deposit.

- Normal Wear and Tear: This is the natural, gradual decline of a property and its fixtures from ordinary, everyday use. This is a cost of doing business that you, the landlord, must absorb.

What Does the "Useful Life" Principle Mean?

Before you charge a tenant for a damaged item, you must consider its "useful life"—the expected lifespan of that item.

You cannot charge a tenant the full replacement cost for a brand-new item if the one they damaged was already old.

Example: A standard carpet has a useful life of about five years. If a tenant causes a large, permanent stain on a four-year-old carpet, you can generally only charge them for the remaining one year of value (20% of the replacement cost), not the full cost of recarpeting.

Types of Tenant Damage

Insurers look first at the cause of damage, then at intent. Frame every claim around the peril, not the tenant’s behavior.

1. Accidental

A pot left unattended ignites a grease fire. Smoke and heat char cabinets and walls. Because fire is a named peril, your policy steps in, less the deductible.

2. Negligent

A tenant forgets to report a leaky fridge line. Water seeps under vinyl planks and warps the subfloor. Insurers treat “sudden and accidental water damage” as covered, yet they expect timely notice, so document your routine inspections.

3. Intentional (Malicious)

Broken bathroom fixtures after an eviction or spray-paint tags are rarely covered. You will rely on the security deposit, civil action, or an optional “malicious damage” or vandalism rider.

Do I Need Landlord Insurance If My Tenant Has Renter's Insurance?

Yes, absolutely. You must have your own landlord insurance policy, even if your tenant is insured. The two policies are not interchangeable because they protect completely different things.

Think of it as covering "your stuff" versus "their stuff."

- Your Landlord Insurance Covers: Your assets. This includes the physical building (walls, roof, flooring), your liability as the property owner, and any items you own inside the unit (like appliances). It also protects you from loss of rent if the unit becomes unlivable due to a covered event.

- Their Renters Insurance Covers: Their assets. This includes the tenant’s personal belongings (furniture, electronics, and clothing) and their personal liability if their negligence causes an accident or tenant damage.

Requiring renters insurance is a smart way to add a layer of protection, but it is not a substitute for your own essential landlord insurance policy.

When Your Policy Pays and What the Adjuster Looks For

Your landlord insurance is designed to be a shield against major financial loss, not a solution for every small repair. Understanding when your policy covers tenant damage can save you time and confusion.

Pro tip: Intentional damage without forced entry—spray-painted walls after a bad breakup, smashed sinks in retaliation—falls outside standard coverage. Add a malicious-damage endorsement or rely on the security deposit to bridge that gap.

What Tenant Damage is Usually Excluded

- Wear and tear or gradual deterioration

- Mold or rot from long-term moisture

- Pet scratches and carpet stains

- Intentional or criminal vandalism (unless you add a malicious-damage endorsement)

- Tenant’s personal items (their renters' insurance applies)

- Loss of rent beyond the “Fair Rental Value” limit

How to File a Landlord Insurance Claim for Tenant Damages

Filing a landlord insurance claim for significant tenant damage requires a strategic, step-by-step approach to maximize your chances of a successful outcome.

Step 1: Mitigate Further Loss and Document Everything

Your first duty under your policy is to prevent the damage from getting worse (e.g., tarping a damaged roof or shutting off the water).

Before making any permanent repairs, thoroughly document the scene with timestamped photos and videos from every angle.

Authoritative Tip: Do not throw away any damaged items, like a burnt appliance or broken fixture. The insurance adjuster must be able to inspect the physical evidence.

Step 2: Review Your Declarations Page & Report the Claim

Find the declarations page of your landlord insurance policy. Review your specific coverages (e.g., for "vandalism" or "fire") and confirm your deductible amount. Then, call your insurer’s claims division number immediately to report the loss.

Authoritative Tip: When you report the claim, you will get a claim number. Write it down and use it in all written communication to create a clear paper trail for your records.

Step 3: Compile Your Complete Evidence Package

Organize all documentation to prove your loss. A thorough evidence package is your best tool to prevent delays and disputes.

Your evidence package must include:

- The complete, signed lease agreement and all addenda.

- The move-in checklist, signed by the tenant.

- All "before" and "after" photos and videos.

- A copy of the police report if the damage was from a criminal act like vandalism. This is non-negotiable for these types of claims.

- Itemized repair estimates from at least two licensed and insured contractors.

Step 4: Consider a Public Adjuster for Major or Complex Claims

For a large-scale or complicated tenant damage claim, you have the right to hire your own licensed public adjuster. Unlike the insurance company's adjuster, a public adjuster works exclusively for you to manage the claim, document the loss, and negotiate the highest possible settlement.

Authoritative Tip: This is a powerful option if your claim is wrongfully denied or the settlement offer is too low. They typically work on a percentage of the claim settlement, providing expert help when the financial stakes are high.

Landlord vs. Tenant Responsibilities When it Comes to Tenant Damages

Negligence test—a court asks four quick questions:

- Duty: Did you have a legal obligation to keep the area safe?

- Breach: Was that duty ignored or handled carelessly?

- Causation: Did the breach directly cause the loss?

- Damages: Are there measurable costs to repair or replace?

If every answer is yes, you, the landlord, end up liable.

Knowing where your duties end and the tenant’s begin helps you prevent claims—and win any negligence dispute that reaches court.

Action Checklist for Plugging Coverage Gaps

1. Tighten Your Security-Deposit Clause

____ Cite the maximum deduction amount (e.g., “up to two months’ rent or the statutory cap, whichever is lower”).

____ List chargeable items like hole repairs, smoke remediation, and appliance replacement so deductions withstand small-claims scrutiny.

____ Require a signed move-in photo inventory; comparing “before” and “after” shots speeds insurer approval and quells tenant disputes.

2. Make Renters Insurance Non-Negotiable

____ Write the requirement directly into the lease and specify a minimum liability limit (US$100,000 is common; US$300,000 is better).

____ Collect the declarations page at signing and every renewal; set a calendar reminder so compliance never lapses.

____ Verify the policy includes liability for property damage to others; this is what reimburses you when tenants cause covered losses.

3. Add a Malicious-Damage (Vandalism) Rider

____ Cost: roughly 5–8 % of your base premium.

____ Covers intentional breakage, kicked-in doors after eviction, smashed sinks, graffiti, and events standard DP forms exclude.

____ Often bundled with “theft” extensions, you get two gap plugs for one endorsement.

4. Layer on an Umbrella Liability Policy

____ Adds US$1–5 million extra protection after the landlord policy limit is exhausted.

____ Crucial when a tenant sues for property loss and bodily injury arising from the same incident (kitchen fire, electrical fault).

____ Premiums start near US$250/year—cheaper than raising base limits on every property.

5. Prove Due Diligence with Routine Inspections

____ Aim for quarterly walk-throughs; some carriers reward premium credits at two visits yearly.

____ Use a mobile app to time-stamp and geotag photos; export a PDF for the policy file.

____ Follow-up letters to tenants (“We noted a slow leak under the sink—please repair within 48 hours”) document that you acted promptly, a key claim-approval factor.

Common Reasons Tenant-Damage Claims are Denied and How to Avoid Them

Even with landlord insurance, a claim for tenant damage can be denied. Knowing the common pitfalls can help you ensure your claim gets approved.

Why Landlord Claims are Often Denied

- The Cause of Loss is classified as an Excluded Peril: Your policy only covers specific perils. Common exclusions that surprise landlords include damage from floods, earthquakes, and often, mold remediation, which may require a separate policy or specific rider.

- Failure to Mitigate Damages: You have a duty to prevent small problems from becoming big ones. If an insurer finds you knew about a minor roof leak and didn't act, they can deny the claim for the major interior water damage that resulted weeks later.

- Damage Is Reclassified as "Wear and Tear": If your documentation doesn't clearly distinguish between tenant abuse and gradual decline, an adjuster will likely classify the issue as non-covered wear and tear.

- Insufficient Proof of Loss: A lack of clear "before and after" evidence means you cannot legally prove the tenant damage occurred during this specific tenancy. The burden of proof is on you.

How to Avoid Landlord Insurance Claim Denial and Protect Yourself

The good news is that you can take simple steps to protect yourself and strengthen any future claims. Being proactive is your best defense against claim denial.

- Conduct Ironclad Inspections: Use a detailed move-in/move-out checklist and supplement it with extensive, timestamped photos and videos. Having the tenant sign the checklist is your most critical tool for legally justifying any security deposit deductions.

- Understand Your Policy's Exclusions: Read your policy to learn what it doesn't cover. Knowing that flood or certain types of animal liability are excluded helps you manage your true risk and avoid filing a claim that is guaranteed to be denied.

- Keep a Property Condition File: For each property, maintain a permanent file with photos of it in pristine condition between tenants, along with receipts for capital improvements (new flooring, appliances, roof, etc.). This helps you establish the property's value and condition before a tenancy begins.

- Provide Prompt, Formal Notice: Always report a potential claim immediately to your insurer's official claims hotline, not just casually to your local agent. This starts the formal process and satisfies your policy's strict notification requirements.

10 Tips for Reducing Damage to Your Rental Property

Taking necessary precautions to protect your rental property from damage is essential. From installing quality locks and security systems to properly maintaining the exterior of the building, there are plenty of ways landlords can reduce the risk of damage to their property.

Here are 10 tips for landlords looking to keep their investment safe.

1. Inspect your property regularly. Check lights, smoke detectors, appliances, pipes and drains, and windows and doors for any signs of wear or damage.

2. Maintain outdoor areas. Trim bushes away from walkways or entryways so potential intruders don't have anywhere to hide. Keep an eye out for overgrown trees that might interfere with power lines or other utility services.

3. Secure windows and doors. Ensure all locks on windows and doors are in good working condition, and consider installing double-keyed deadbolts for extra security.

4. Install a security system. This system could be a simple alarm that goes off when a door opens to more advanced options with motion detectors, cameras, and other surveillance measures.

5. Check references of potential tenants. When screening new tenants, perform a thorough background check before signing the lease agreement, including credit history, criminal record, rental history, employment, and income verification. While this may seem obvious, it can be surprising how many landlords don’t conduct a comprehensive tenant screening process.

6. Educate tenants on safety measures. Provide tenants with a checklist of safety tips and precautions they should take while living in the rental property. This list might include keeping doors locked at all times and notifying you immediately if they see any signs of damage or wear.

7. Offer tenant incentives for taking care of the property. Some landlords may offer reduced rent to tenants who keep their rental clean and tidy or other bonuses for maintaining the building’s exterior.

8. Set clear guidelines in the lease agreement. Be sure your tenants understand what is expected of them when taking care of the property by including detailed descriptions in the lease agreement.

9. Take preventive action. If you notice any signs of potential damage to the property, such as a leaking roof or broken windows, take care of it right away before it gets worse and becomes more expensive to repair.

10. Adequately insure your property. Talk to your insurance agent about any additional protection you may need for your property, such as flood insurance or liability coverage.

Lock In Coverage Before Tenant Moves

Protect cash flow, property, and peace of mind with Obie’s purpose-built landlord insurance. In minutes, answer a few questions online and receive a custom quote that covers tenant damages and more. See transparent pricing, no phone tag, no hidden fees. Get started now—request your free quote today and feel confident every lease period is backed by expert support with zero obligation today online.

FAQs about Landlord Insurance and Tenant Damages

What is the difference between malicious and accidental tenant damage?

Malicious damage is when a tenant intentionally destroys your property. Think of it as vandalism, like punching holes in walls or smashing fixtures.

Accidental damage is unintentional, like a kitchen fire from a cooking mistake or a deep scratch on the floor from moving furniture.

Your landlord insurance is more likely to cover significant malicious damage, while coverage for accidents can vary by policy.

Should I use the security deposit or file an insurance claim for tenant damage?

For minor issues like a stained carpet, a broken cabinet door, or small holes in the wall, it is almost always better to use the security deposit. This is faster and avoids a potential increase in your insurance premiums.

For major, costly tenant damage like a fire or significant vandalism where repair costs far exceed the deposit, you should file a claim with your landlord insurance.

Does landlord insurance cover lost rent if a tenant damages the property?

Often, yes. Most comprehensive landlord insurance policies include "Loss of Rent" or "Rental Income Protection." If a covered peril (like a fire or major water damage caused by a tenant) makes your property uninhabitable, this coverage helps pay for the lost rental income while the unit is being repaired. It does not cover lost rent if a tenant simply stops paying or breaks their lease.

Can I make a tenant pay my insurance deductible?

You can include a clause in your lease agreement stating that the tenant is responsible for the insurance deductible if their negligence leads to a claim.

However, the enforceability of this clause depends on local landlord-tenant laws in your area, such as those in the Philippines. consulto consult with a legal professional to draft a compliant lease.

Does landlord insurance cover the cost of an eviction?

No, a standard landlord insurance policy does not cover the legal fees or administrative costs associated with evicting a tenant. Insurance is designed to cover property damage and liability, not legal proceedings related to the lease agreement itself.